The P&L was the moat

AI broke the cost structure that protected banks. Stablecoin rails are only the entry point. I spent the last several years telling founders not to start banks. I was right. Now I might be wrong.

Not because banking became easy. It didn’t. Not because licenses stopped mattering. They still do. Not because stablecoins magically turn a fintech wrapper into a bank. They don’t. The reason is simpler and more uncomfortable.

The thing that protected banks was never the product. It was the P&L.

That moat is breaking.

I worked on two banks - Revolut Business and Monzo Business. Then I spent a couple of years consulting a dozen more, seed to Series D, retail and SMB, Europe and US. Most had better teams than the ones winning. Most had better ideas. Almost none broke through.

They didn’t lose on product. They lost on the P&L. Dozens of teams are now building banks on stablecoin rails. Most are still pitching the same story challengers have pitched for a decade: better UX, faster settlement, novel rails, programmable money. That story is not wrong. It is incomplete.

New rails lower the cost to launch. AI lowers the cost to operate. The second is the bigger shift.

The market was closed for a reason

The moat that killed every challenger I worked with after Series B wasn’t product. It was economics.

I watched this from several angles. Monzo against Revolut. Then later, other founders against Revolut and the high street. Many had better products. Some had meaningfully better products. They cleared seed and Series A on momentum, taste, and user love. Then somewhere around Series B, the same thing happened: CAC stopped pencilling.

The incumbent could pay more for the same customer. That was the whole game.

The incumbent had the lending book, interchange volume, deposits, cross-sell, sponsor-bank relationships, compliance machinery, risk team, brand and balance sheet.

A challenger could win the interface and still lose the customer.

Because banking acquisition is an auction. The cost-per-acquired-customer is set by whoever can pay the most. Whoever can pay the most is whoever has the best unit economics.

Revenue per customer. Cost-to-serve. Risk cost. Compliance cost. Funding cost. Cross-sell. Retention. Recovery. That was the moat. Not the app. Not the card. Not the onboarding flow. The P&L.

The cost base just changed

Banks are operational pipelines with a software wrapper. A large share of bank OpEx is personnel. A meaningful chunk of that personnel does rule-bound work: KYC and KYB analysts, compliance officers, support agents, fraud reviewers, onboarding teams, dispute-resolution staff and internal operations.

AI does specifically that kind of work. Not perfectly. Not autonomously end to end. Not without escalation, audit, and human judgment. But enough to change the shape of the cost base. The asymmetry matters.

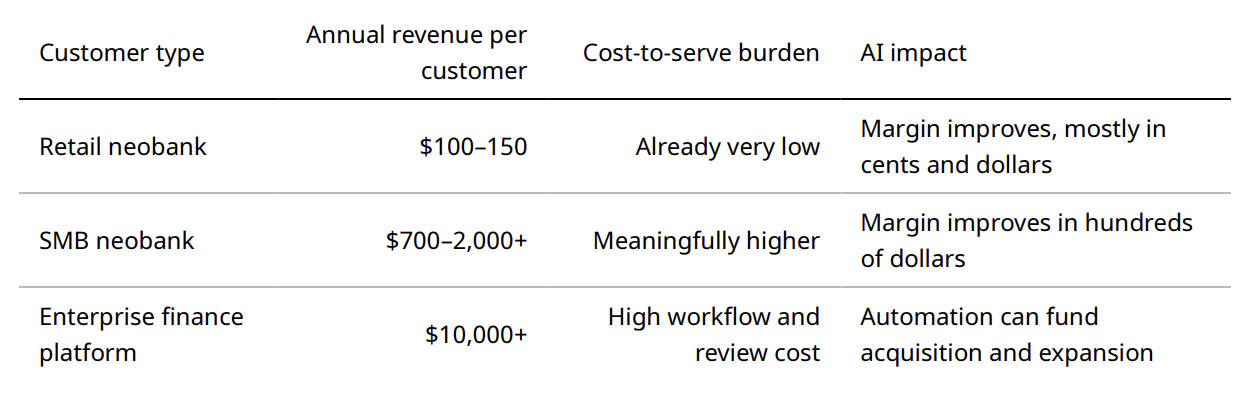

A retail neobank customer may be worth tens of dollars a year. Cost-to-serve is already tiny. At that scale, AI helps. It improves margin. It reduces support burden. It compounds across hundreds of millions of users. But the absolute dollars per customer are small.

An SMB customer is different. Revenue per customer is higher, and the operating burden is heavier: commercial onboarding, KYB, sanctions checks, beneficial ownership review, fraud monitoring, support, reconciliation, approvals and exception handling. That is where AI has leverage.

The same automation that saves a retail bank dollars can save an SMB bank hundreds. Same automation. Different ARPU. That is the opening.

The simple model

Take an SMB banking customer worth roughly $2,000 a year in revenue.

If the bank runs at a 60% cost-to-income ratio, it has $800 of contribution before acquisition. If AI compresses operating costs by 20–30%, that creates roughly $240–360 of extra room per customer. That room can go three places: margin, pricing, or acquisition.

In consumer banking, the same percentage improvement is real but smaller in absolute dollars. If a retail customer generates $100–150 a year and costs less than $1 a month to serve, AI still helps. But it helps in cents and dollars. In SMB banking, it helps in hundreds.

This is the part most “bank on stablecoin rails” pitches miss. The rails lower the cost to launch. AI lowers the cost to operate. The second matters more.

The proof is already in the system

The compression is visible, even if the maximalist version is wrong.

Klarna is the warning label. Its AI assistant handled two-thirds of customer-service chats in its first month, reduced resolution times from 11 minutes to under 2, and was projected to improve profit by $40M. Then came the walk-back: the company had pushed too far and needed more humans back in the loop for service quality.

That does not kill the thesis. It sharpens it. AI does not remove the need for humans in regulated financial services. It changes where humans sit in the system.

Ramp is the cleaner SMB data point. Its agents catch more out-of-policy spend, reduce manual expense reviews, and automate work that used to sit with finance teams. This is not chatbot theater. It is rule-bound operating work moving into software.

Now apply that across the bank stack: KYC, KYB, onboarding, fraud review, sanctions screening, disputes, support, reconciliation and internal tooling.

Not to zero. Never to zero. But down.

A new rail changes settlement. A new cost base changes the P&L.

The rails are not the bank

What used to require tens of millions in capex and years of regulatory work now sits on a shelf. Stablecoin orchestration, virtual accounts, wallets, on/off-ramps, card issuing, ACH, SEPA, wires, FX, ledgering, KYC, KYB, sanctions screening and compliance tooling are increasingly API layers.

That is good news. It is also a trap.

If everyone can rent the rails, the rails are not the moat.

A lot of “stablecoin banks” are thin wrappers over rented infrastructure. That may be enough to launch. It is not enough to win.

The rails are not the bank. The rails commoditise. The operating system, if you build it right, does not. So the question for any new entrant is not: what rails are you on? It is: what does your operating cost base look like once you have actually built this thing?

The incumbents are awake

The strongest counterargument is obvious: the incumbents see this too.

They do. Revolut, Starling, NatWest, Klarna, Mercury, Ramp and every serious bank or fintech are already working AI into the stack. Nobody in this category is asleep.

But this is exactly what happened with digital transformation. Some incumbents nailed it. Most did it slowly and badly. A decade and a half later, plenty of high-street banks still ship apps anyone under 35 finds frustrating.

AI transformation will rhyme. The largest banks will have the budget, the data and the internal talent. They will also have legacy cores, compliance drag, internal politics, fragmented systems, procurement cycles, risk committees and products built for a pre-agent world.

For the duration of the transition - measured in years, not months - there is a structural arbitrage. A bank built from scratch on an AI-native cost base, on modern rails, with a development substrate built for agents, can spend more on customer acquisition than mid-tier competitors and still print margin.

The window is finite. Five years. Maybe ten. But it exists.

The next bank may not look like a bank

This is where the “stablecoin bank” framing starts to feel too small.

If the old bank was a consumer interface wrapped around a balance sheet, the next bank may be an operating layer for autonomous workflows. Vertical agents will source suppliers, approve invoices, reconcile orders, manage cash, trigger payouts, and resolve exceptions. At some point, every workflow that manages work will also need to move money.

That is a different demand surface.

The customer may not start by asking for a bank account. They may ask for an agent that runs procurement, pays contractors, manages freight or closes the books.

The financial product becomes embedded inside the workflow and the workflow becomes the distribution.

That is why the rails are only the entry point. The real company is the control layer: permissions, counterparties, approvals, audit, reconciliation, memory and policy. In a world where agents initiate more work, finance becomes less like a destination app and more like an execution protocol.

That is the bank for vertical agents.

The market is open again

I spent the last several years telling founders not to start banks. The market was closed for a reason. The winners had better economics. The challengers had better slides.

That is changing. Building a bank is possible again - retail or SMB, in any geography where the regulated infrastructure is rentable. Not easy. Never easy. But possible in a way it genuinely was not five years ago.

Just being cheaper to run is not enough. A bank that only clones an existing product with better margins can make money. It will not build a category.

The companies that win this round will combine three things:

- AI-native cost base: lower operating cost, faster reviews, tighter controls, fewer manual queues

- Modern rails: stablecoins, instant settlement, API-native treasury, programmable accounts

- New demand surface: vertical AI agents, autonomous workflows, embedded finance, and businesses that expect money movement to be part of software

Where the next moat is - what defends a bank in a world where cost structure no longer does - is the next piece. Until then: it stopped being a closed category.

The P&L was the moat. AI broke it. The market is open again.